The problem is not just local, it is worldwide. Again and again, the belief has been proven wrong that central bankers could guarantee so-called price stability, and that fiscal policy could prevent economic downturns. The looming inflationary crisis is one more piece of evidence that interventionist monetary and fiscal policies are disruptive. Instead of a permanent boom, explains Antony Mueller in this guest post, the result is stagflation....

Stagflation—a Keynesian Curse

Guest post by Antony Mueller“Stagflation” characterises economies that are plagued by inflation, combined with economic stagnation. This is where most of the world is right now, because of the failed (and failing) economic policies they have all followed. In this case, the conventional Keynesian macroeconomic toolkit of monetary and fiscal policy, that offers no help in fixing the crisis it has caused.

Rising price inflation rates and tanking economies are the results of the policy mix that has dominated past decades. It has become common to believe that decades of expansive monetary and fiscal policies would not cause price inflation; that the expansion was 'all under control'; that policies of so-called price stability had somehow 'tamed' the inflation caused by the state's usual money printers.

As recently as 2020, economic policy worldwide followed the false consensus that combatting the fallout from the lockdowns with additional money creation and higher government spending would lead to an economic recovery without higher price inflation. It was blithely assumed that what appeared to work in 2008 -- flooding economies with newly-minted cash -- would also function in 2020. However, policymakers ignored the difference between the two episodes.

In the aftermath of the financial crisis of 2008, the stimulus policies did not immediately turn into price inflation, as it's commonly measured, because the newly-created money remained largely in the financial sector and it only spilled over into the real economy in a big way in rocketing house prices (exacerbated in NZ by sclerotic land and housing policies). Outside of this generational calamity, the main effect of the policy of low interest rates was to support the stock market and to provide a windfall to financial investors. While Wall Street flourished, Main Street was left on the sidelines -- and while profits surged, wages remained stagnant.

But this time it's different. In 2008, the production side of economies were 'mismatched' due to the earlier credit expansion, but still intact; but this time, they are severely damaged by a major pandemic. The crisis of 2008 left the capital structure of the real economy intact. Due to the lockdowns, however, this is no longer the case. Consequently, severe interruptions of the global supply chains have happened. In such a constellation, new stimulus measures further weaken already fragile economies.

In the aftermath of the financial crisis of 2008, the stimulus policies did not immediately turn into price inflation, as it's commonly measured, because the newly-created money remained largely in the financial sector and it only spilled over into the real economy in a big way in rocketing house prices (exacerbated in NZ by sclerotic land and housing policies). Outside of this generational calamity, the main effect of the policy of low interest rates was to support the stock market and to provide a windfall to financial investors. While Wall Street flourished, Main Street was left on the sidelines -- and while profits surged, wages remained stagnant.

But this time it's different. In 2008, the production side of economies were 'mismatched' due to the earlier credit expansion, but still intact; but this time, they are severely damaged by a major pandemic. The crisis of 2008 left the capital structure of the real economy intact. Due to the lockdowns, however, this is no longer the case. Consequently, severe interruptions of the global supply chains have happened. In such a constellation, new stimulus measures further weaken already fragile economies.

The present situation is less like 2008, which most of of us still remember, and more like the oil price shock in 1973 -- which too many current economic practitioners and advisers have forgotten. At that time, like now, the external shock hit an economy rampant with liquidity. Stimulating the economy by fiscal and monetary expansion produced not prosperity but long-lasting stagflation. Back then, along with “stagflation,” the term “slumpflation” was coined to characterise an economy that is mired in a deep slump that then gets devastated by price inflation.

When stagnation and recession show up together with price inflation, the conventional macroeconomic policy becomes impotent. Applying the Keynesian recipe to an economy whose capital structure is still intact inflates bubbles; but applying it to one who capital structure has already been ravaged invites disaster.

Intentionally or by ignorance, policymakers neglected the long-term effects of their doing. Going this wrong way led to such aberrations that policymakers and their intellectual bodyguards even tended to believe that some truth could be found in the alchemy of the so-called modern monetary theory and market monetarism.

The consequences of these policy errors have now come to light. They are particularly grave because they were committed by all major central banks and the governments of all leading industrialised countries. They all follow the concept of “inflation targeting.” Other than timing, there has been not much difference among the policies of major Western economies. Japan is a special case only insofar as its policymakers have applied the Keynesian recipe for over three decades by now.

Let us have a look at Japan first and then at the United States -- who both offer lessons for New Zealand.

Japan

Japan began applying vulgar Keynesianism as early as in 1990. Faced with a slight downturn after the boom of the 1980s, instead of allowing things to cool down, the Japanese leadership instead insisted on going on with the show.

Yet, the more the government began to accelerate public spending and increases the fiscal stimuli, the less its spending policy produced economic recovery. Even when monetary policy fully supported the government’s expansive fiscal policy, the hoped-for recovery did not materialise.

John Maynard Keynes, on whose theories this "rescue" was based, once advised that policy-makers should ignore advice that such loose spending would lead to destruction in the long run -- "in the long run," he quipped, "we're all dead." But Japan's short run is now the long run: its policy mix of fiscal and monetary expansion has been going on now for three decades. In recent times, the Bank of Japan even doubled down, setting extremely low-interest rates and finally resorting to negative interest rates (NIRP). In the meantime, public debt as a percentage of the gross domestic product (GDP) rose to a whopping 266 percent (see figure 1).

Figure 1: Japan: Policy interest rate and public debt as a percent of GDP

Source: Trading Economics.

Despite its magnitude, this stimuli did not lift the Japanese economy out of its quagmire. Instead, economic growth remained anemic for a quarter of a century (figure 2).

Figure 2: Japan: Annual economic growth rates of real GDP

Source: Trading Economics.

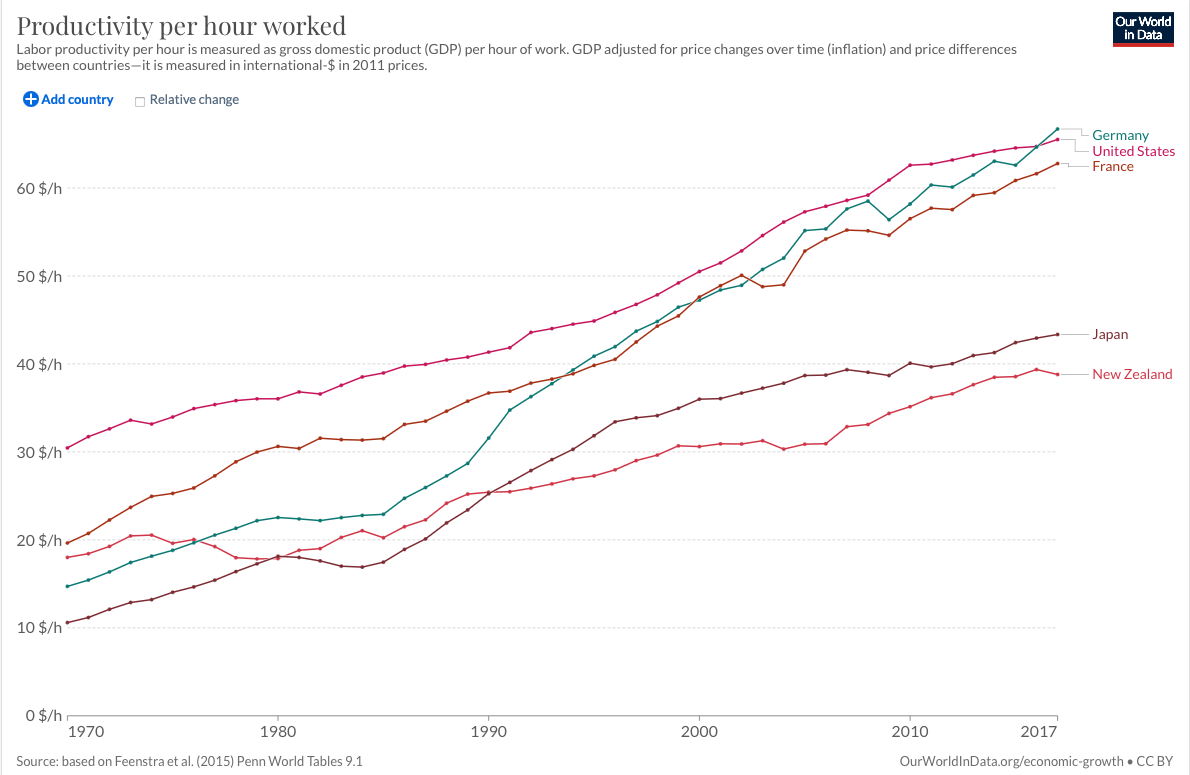

As an “early starter” in applying vulgar Keynesianism to its 'macroeconomy,' the Japanese economy was also early to suffer from productivity stagnation. Unlike economies like the United States, France, Germany, and many other industrialised countries, which have continued with productivity gains over the past decades, after it had begun with its extreme Keynesianism in the 1990s Japan's has moved sideways (and New Zealand, for slightly different and equally tragic reasons, has followed a similar path -- figure 3).

Figure 3: Productivity per hour worked: Germany, United States, France, Japan, New Zealand

Source: Our World in Data.

It is important to note that one of the most devastating effects of the Keynesian policy mix is its effect on productivity. A country’s long-run economic progress (or growth, as it's often called) is mostly the result of productivity gains. Labour productivity is the main determinant of wages. A slowdown in productivity precedes the economic decline. When the output per unit of input tends to fall, even lower interest rates will not stimulate business investment. The marginal productivity of debt, already low, diminishes even faster -- and further.

And when government then jumps in to compensate for this “lack of aggregate demand,” things get even worse because governmental enterprises are fundamentally less productive than the private sector.

Confronted with the financial crisis of 2008, the US government abandoned any sense of economic responsibility and decided instead to launch a series of stimulus packages. The American central bank provided full support, drastically reducing its interest rate.

The United States

Confronted with the financial crisis of 2008, the US government abandoned any sense of economic responsibility and decided instead to launch a series of stimulus packages. The American central bank provided full support, drastically reducing its interest rate.

As a result, the ratio of public debt to GDP rose from 62.6 percent (in 2007) to over 91.2 percent just three years later (in 2010), reaching a full 100.0 percent in 2012. The next two boosts came in the wake of the policies to counter the effects of the economic lockdowns, when the ratio of public debt to GDP rose to 128.1 percent in 2020 and to 137.2 in 2021 (see figure 4). It took less than fifteen years to more than double an already barely-sustainable debt -- and, unfortunately, New Zealand governments chose a similar destructive trajectory.

Figure 4: The United States: Policy interest rate and federal debt as a percentage of GDP

Figure 4a: New Zealand: Policy interest rate and government debt as a percentage of GDP

Source: Trading Economics.

In the face of the crisis in 2008, the American central bank brought down its interest rate quickly from over 5 percent in 2007 to under 1 percent in 2008 (NZ's meanwhile dropped its rate from 8% to 2.4% over the same period). After a short-lived period when the American central bank tried to raise the interest rates, the consequent market reaction of falling prices of bonds and stocks induced the Fed to resume its policy of “quantitative easing” that combined low interest rates with the massive expansion of the monetary base.

Then, in early 2020, still trying to escape from the bear-trap of quantitative easy, it also began trying to "ease" the economic effects of the lockdowns with its patent brand of monetary salve, deciding to continue with its expansive monetary policy. And not just to continue, but to accelerate! In due course, the central bank’s balance sheet rose to $7.17 trillion in June 2020, reaching $8.96 trillion by April 2022. Once again, New Zealand's Reserve Bankers followed the lead.

Figure 5: Balance sheet of the US Federal Reserve System & NZ Reserve Bank

Source: Trading Economics.

As figure 5 shows, the Fed had tried to trim its balance sheet somewhat from 2015 to 2019 when it had brought down the sum of its assets to $3.8 trillion in August 2019. Yet beginning already in September 2019, many months before the lockdown was implemented, the balance sheet of the American central bank began to expand again and reached over four trillion before the additional big increase happened due to the fallout from the lockdowns. (And, once again, NZ's central

Since the time before the financial crisis of 2008, the assets of the Federal Reserve System rose from $870 billion in August 2007 to a whopping $4.5 trillion in early 2015 and to around nine trillion US dollars in early 2022.

Even when inflation rates began to rise towards the end of 2020, the US central bank had kept its policy of tapering small and refrained from tightening. The monetary authorities had simply abandoned the objective of reining in the money supply, becoming instead almost Wall Street's banker. Each time they tried to tighten monetary policy, the financial markets began to tank and tended to crash. As soon as the central bank began to raise its policy rate of interest, the bond market began to tank and took the stocks down with it. In 2022, it was not different. Yet in early 2022, the policymakers could not shrink back. Different from the episodes before, the price inflation had begun to skyrocket (see figure 6, and NZ following in almost lockstep, figure 6a).

In the first months of 2022, stagflation became fully visible. While price inflation rose, the rate of real economic growth began to fall. In the first quarter of 2022, the US inflation rate moved up to a rate of 8.5 percent, while the real annual growth rate fell by 1.4 percent. Similar things were happening in the South Pacific.

Figure 6: United States: Policy interest rate and official consumer price inflation rate

Figure 6a: New Zealand: Policy interest rate and official consumer price inflation rate

Of course, none of this should come as any surprise. With global supply chains in disarray, and national protectionism on the rise, the assistance that came from the expansion of international commerce after the crisis of 2008 is no longer with us. The lockdown of economies has severely hurt the global system of supply chains -- and now, a huge monetary overhang meets a shrinking production. The war in Ukraine, which started in February 2022, is not to blame for the distortions, albeit it will make them more severe.

Conclusion

The levee broke. Price inflation is on the rise. This is the result of the accumulation of liquidity that has been going over decades. There is the risk that things will get worse because the world economy has been severely wounded by the lockdown. More so than only mild stagflation, a “slumpflation” looms on the horizon as the world economy gets mired in the morass of a deep slump combined with steeply rising price inflation.

But the problem was not inevitable -- it is a result of specific policies followed out on the basis of flawed economic theory. Local politicians are right in one way to blame the problem on global issues -- the problem is that this destructive Keynesianism is everywhere, and as long has it is, so will the problems.

* * * *

Author: Dr. Antony P. Mueller is a German professor of economics currently teaching in Brazil. See his website and blog. A version of this post previously appeared at the Mises Wire.

No comments:

Post a Comment